Frax Finance; an Algo-Stable Above the Rest

Frax Finance has quietly become the largest DAO holder of CVX tokens, while expertly executing a brilliant strategy to set them up as a dominant force in the Curve Wars and DeFi ecosystem at large.

Introduction

While the Curve Wars have gathered an immense amount of attention as people begin to understand how pivotal Curve is in the entire DeFi ecosystem, there are several layers to what is truly happening in this battle for liquidity. Many stablecoin projects have benefitted considerably from the incentive structures surrounding the Curve/Convex ecosystem, but one stablecoin project, in particular, has risen above the rest: Frax Finance.

Stablecoins, specifically algo-stables have found a great amount of utility in Curve and Convex. To help bootstrap liquidity, algo-stables such as FRAX have been bribing CVX holders to keep giving their gauge votes towards the FRAX pools. This gives the CRV emission to them, and there are several ways to gain revenue from this.

Sell the CRV emissions earned at market price

Lock CRV on Curve and receive nontransferable veCRV gov power (plus LP bonus) to help direct Curve gauge votes to your pools

Lock CRV on Convex and receive maximum yield, transferable crvCVX, and CVX emissions that can help direct Curve gauge votes to your pools

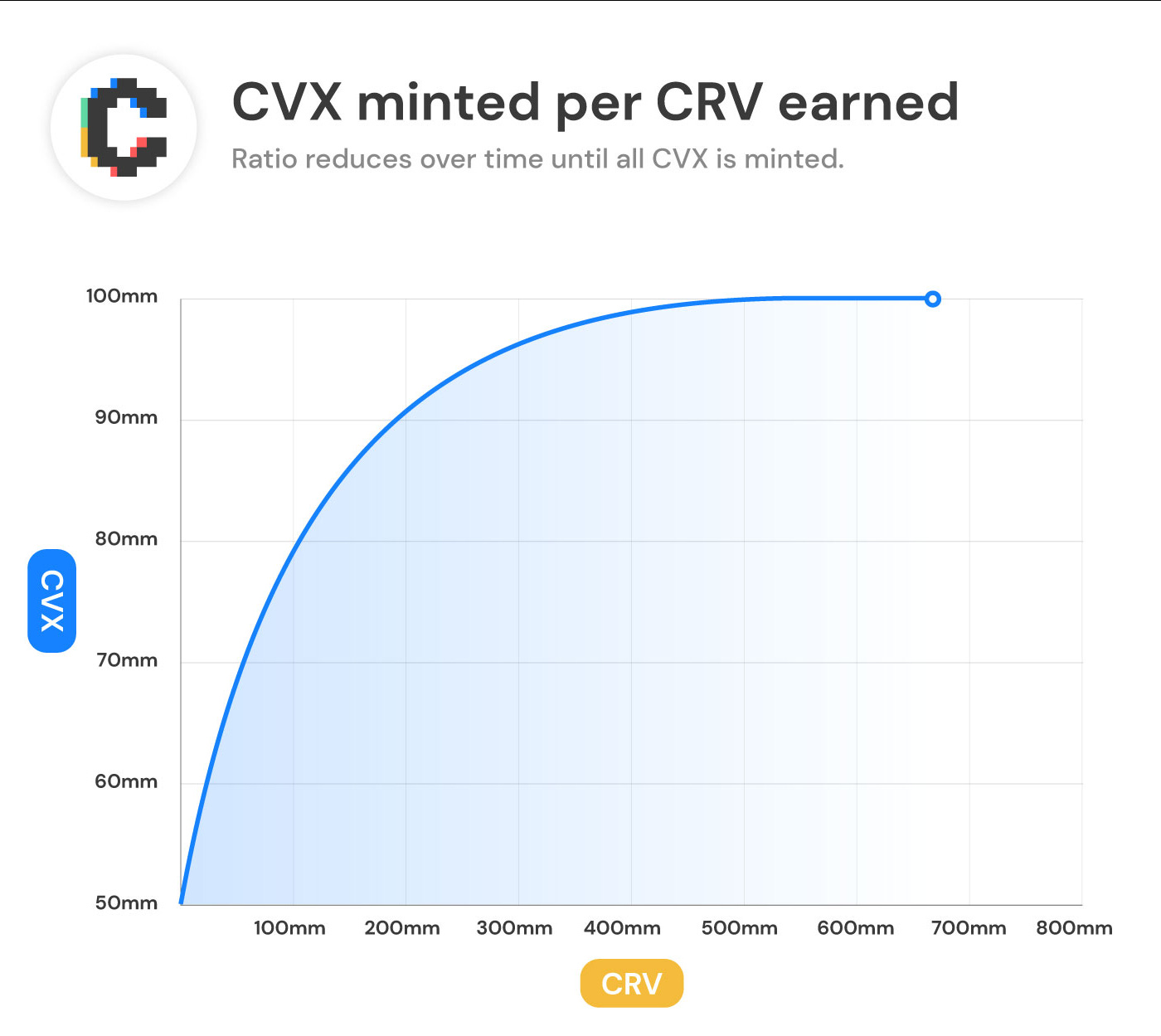

While this is a solid shorter-to-medium-term strategy, this can only work for so long. The CVX emission schedule is such that it decreases as more CRV is locked on the protocol, bringing scarcity to the asset (see chart below).

Playing the Long-Game

In addition, stablecoin projects need to provide utility to have a product-market fit. What does this look like? Well, stablecoins have the inherent utility of providing stability to the DeFi ecosystem. This means becoming the denominating asset for swap pools, and ideally lending and borrowing eventually as well.

To help bootstrap liquidity, Frax Finance has been playing the Curve/Convex ecosystem extremely well. Frax Finance was one of the first DAOs to begin acquiring CVX tokens hoping to sway inflationary rewards to themselves through the gauge weight votes. At the time of writing, they hold roughly 1.6 million CVX tokens, roughly 3% of the entire circulating supply. When looking at the data, the road to becoming the DAO that holds the most CVX looks like it was a smooth ride for Frax Finance, but maintaining that top spot may prove difficult. As you can see in the chart below, many DAOs will acquire a lot of CVX at once, such as Redacted Cartel, Terra, and Mochi.

Gauging Interest

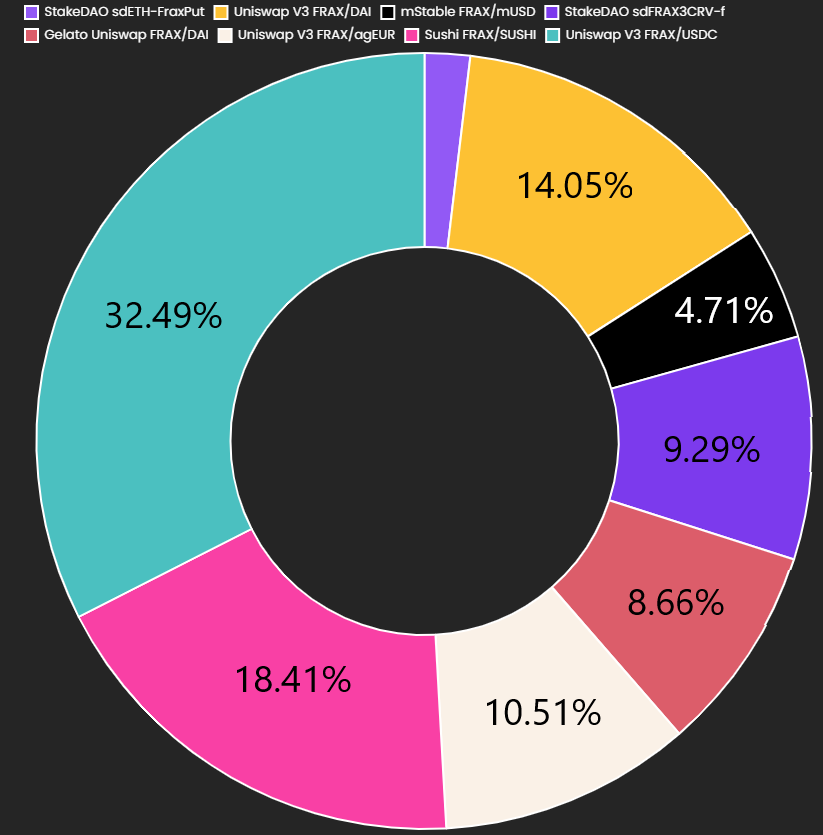

Frax Finance fits better into the Curve/Convex ecosystem better than most, and this is mainly due to its unique token design. Frax Finance has a two-token design: FRAX, the decentralized stable coin, and FXS, the governance token behind it. Similar to Curve, Frax has adopted the VE (vote escrow) governance model. While the veCRV holders dictate gauge weights on Curve inflationary emissions, veFXS vote on gauges that dictate FXS emissions. The main difference here: Curve emissions are rewarded across the DEX pools on Curve, while FXS emissions are paid out to various trading pools on different DEXs. For example, the largest current receiver of FXS emissions is the Uniswap V3 FRAX/USDC pool, with 32.49% of emission rewards. Essentially, veFXS gauges are the money-layer gauge weights of DeFi while Curve gauge weights are the DEX-layer weights.

The value proposition for these trading pools to receive FXS emissions is clear. With FXS emissions they can do a number of things:

Stake their emissions as veFXS to receive more voting power to ensure they continue receiving more FXS

Redeem their FXS for FRAX which would deepen the liquidity on their pool, tighten the spread, improve the price for users, and theoretically drive more volume

Lastly, they can hold FXS in a spot position, or stake it elsewhere.

Unlike Curve, where there is not currently a plan of what will happen when the community emissions run out, FXS emissions will be converted to FRAX emissions once the 60m FXS at a rate of 25k a day run out.

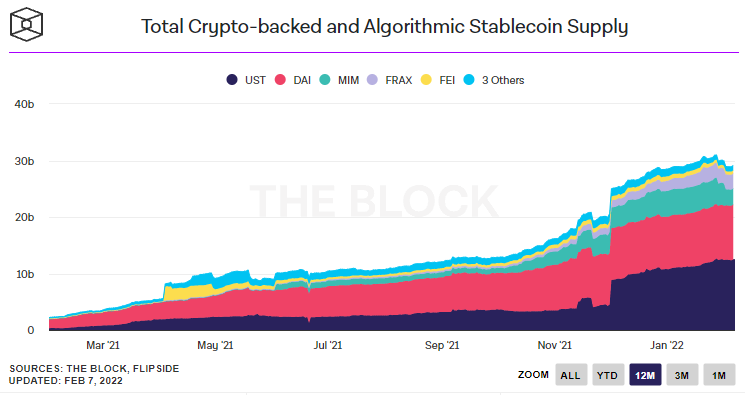

Frax Finance has an emission model which is much more useful in the distribution of unlocking the true potential of their own tokenomics. Frax will ultimately be a success if it is distributed across as many DEXs on as many chains as possible, preferably as the denominator asset in a trading pair. From there, it will then likely look to also be involved in lending protocols. However, accomplishing the first task is much harder than it looks. There is a competitive market for algo-stables, as we’ve seen the collective market cap balloon to roughly $30bn in the past year.

Frax Supply & Burn Mechanism

FRAX in particular has seen a rapid rise to just under a $3 billion supply in only 2 years. The name FRAX means fractional, where the token itself is collateralized by several digital assets. The algo-stable’s peg is maintained by burning FXS from the supply when the FRAX algo-stable is under the 100% collateralization ratio. At the time of writing, the collateralization ratio is 84.50%, which means that to print $10m new FRAX, 10m/(current price of FXS) FXS would have to be burned from the supply. This means when FXS is at a lower price, more of it is burned in order to mint FRAX; an important and intentional part of the tokenomics.

FXS on Convex

Recently, FXS has been increasingly hard to come by for two main reasons. The first is their recent integration on Convex. It’s important to understand how deeply intertwined these two protocols truly are. As stated earlier Frax Finance has been slowly acquiring CVX by staking their CRV emissions on Convex Finance. This in turn has produced a flywheel effect for them where they have been able to lock their CVX tokens on Convex and have more control over the gauge weight votes, where they have been able to earn more CRV emissions and continuously repeat this process. This recent integration has allowed users to lock FXS on Convex and receive cvxFXS in return. Convex stated that vlCVX holders will then be able to vote on FXS gauge weight votes. This formation of a sophisticated bribe market will help in directing FXS emissions to the LPs of trading pools willing to pay the most for it, much like what has happened to Curve’s CRV token. Thus far, we have seen over 3m (3%) of the total supply of FXS become locked on Convex, forever.

TokeMak; Liquditiy Directed

The second area of interest for Frax Finance is Tokemak. Tokemak is a protocol intended for the distribution of liquidity governed by TOKE holders. Frax Finance recently approved a proposal that aims to allocate up to 100m FRAX to its Tokemak pair reactor. Much like the synergistic relationship, Frax has formed with Convex; Tokemak offers a similar opportunity. Given the structure of FXS gauge rewards going to DEXs, every asset that is deployed with a FRAX pairing becomes potentially eligible for emission rewards. In addition, this leads to a possible scenario where Frax Finance accumulates TOKE to increase its reserves and corresponding pairings within Tokemak, and Tokemak could continue to accumulate FXS, lock it as veFXS and vote on its own Frax gauge weights. Lastly, Tokemak can then bribe vlCVX holders to vote on their own Frax pairings to further optimize the gauge weights associated with them.

Tokemak offers liquidity as a service, a novel concept in DeFi. Analogous to the Curve situation where votes dictate gauge weights, the TOKE votes determine where liquidity will be routed. For example, if you are a TOKE staker, you can vote where to route liquidity. Who needs this liquidity? Decentralized exchanges. More liquidity, lower spreads, better prices, more volume, especially when considering aggregators are making the choices now. (Matcha, 1Inch, 0x)

The more liquidity a pool receives with a decentralized stable such as FRAX, being the denominating asset, the more utility FRAX then has, and a positive feedback loop of adoption occurs. There is currently 8.5m FXS being staked on Tokemak, 183% more than the amount locked on Convex, second only to veFXS in terms of categorization.

Conclusion

In conclusion, Frax Finance is making all the right decisions from a protocol standpoint. A truly decentralized stable coin is necessary to foster a truly decentralized financial system. The vision and execution of being the first DAO to strategically accumulate CVX has served them well, and FXS’ integration into Convex will deepen the dominant position Frax Finance has carefully crafted. The TokeMak synergies and partnership will help bring deeper FRAX liquidity to many different DEX pools on a variety of chains, extending FRAX’s reach far and wide. Frax Finance is a sleeping giant with a clear long-term vision, their execution has been to a tee thus far, and I wouldn’t count on them slowing down anytime soon.

Sources

Frax Finance documentation

Tips Welcome: unsworth.eth

Disclaimer: This Content is for informational purposes only, you should not construe any such information or other material as legal, tax, investment, financial, or other advice.